![HITV APP Download [Apk] Latest Version [Unlimited Movies]](https://hitvofficial.com/wp-content/uploads/2024/06/cropped-HiTV-Official-3.png)

The Role of Fraud Prevention Tools in Securing Transactions

In the digital era, businesses process millions of online transactions daily. While this shift to digital payments has made commerce more efficient, it has also opened the door to cyber threats, fraud, and financial crimes. Fraudulent transactions cost businesses billions of dollars annually, making fraud prevention tools a necessity.

Fraud prevention tools help businesses detect and stop suspicious activities before they result in financial losses. From real-time monitoring to artificial intelligence-driven risk assessments, these tools are essential for safeguarding businesses and customers alike. This blog explores the importance of fraud prevention tools, how they work, and their role in securing digital transactions.

Understanding Fraud in Online Transactions

Online fraud takes many forms, with cybercriminals constantly evolving their tactics. Businesses that process payments online face several fraud risks, including:

1. Card-Not-Present (CNP) Fraud

CNP fraud occurs when a fraudster uses stolen credit or debit card details to make online purchases. Because the card is not physically present for verification, businesses must rely on fraud prevention measures to detect unauthorized transactions.

2. Chargeback Fraud

Chargeback fraud, also known as “friendly fraud,” happens when a customer makes a legitimate purchase but later disputes the charge, falsely claiming they never received the item or did not authorize the transaction. This type of fraud results in revenue losses for businesses and increased operational costs.

3. Account Takeover Fraud

Cybercriminals use stolen login credentials to gain access to a customer’s account and make unauthorized purchases. These attacks often involve phishing scams or credential-stuffing techniques, where hackers use previously leaked passwords to access multiple accounts.

4. Synthetic Identity Fraud

In this type of fraud, criminals combine real and fake personal information to create new identities. These synthetic identities are then used to open accounts, apply for credit, or make fraudulent transactions.

To combat these threats, businesses need fraud prevention tools that analyze transaction patterns, detect anomalies, and prevent fraudulent activities in real time.

How Fraud Prevention Tools Work

Fraud prevention tools use advanced technologies to analyze transactions and identify suspicious activity. These tools operate through various mechanisms, including:

1. Machine Learning and Artificial Intelligence (AI)

AI-driven fraud prevention tools analyze vast amounts of transaction data to detect unusual behavior. Machine learning algorithms continuously improve by identifying patterns that indicate fraud.

For example, if a customer typically makes purchases from the U.S., but a transaction suddenly appears from an unfamiliar location, AI-powered tools can flag it as suspicious. The system may then request additional verification or block the transaction altogether.

2. Real-Time Transaction Monitoring

Real-time monitoring tools track transactions as they happen, identifying high-risk payments instantly. These tools use predefined rules, such as checking for sudden spikes in transaction values or multiple failed payment attempts.

If a transaction appears suspicious, businesses can take immediate action, such as requiring multi-factor authentication (MFA) or temporarily freezing the account until further verification is completed.

3. Behavioral Analytics

Behavioral analytics tools track user behavior to detect anomalies. These tools analyze how customers typically interact with a website or app, including their login patterns, typing speed, and navigation habits.

If a customer suddenly exhibits unusual behavior—such as logging in from multiple locations within a short time—fraud prevention tools can trigger security alerts.

4. Device Fingerprinting

Every device has a unique digital fingerprint based on its hardware, software, and network attributes. Fraud prevention tools use device fingerprinting to identify trusted devices and flag unfamiliar ones.

For instance, if a customer consistently shops using a laptop but suddenly attempts a high-value purchase from a new mobile device, the system can request additional security checks.

5. Multi-Factor Authentication (MFA)

MFA adds an extra layer of security by requiring users to verify their identity using multiple credentials. This could include a combination of:

- Passwords

- One-time passcodes (OTP) sent via SMS or email

- Biometric verification (fingerprint or facial recognition)

MFA makes it harder for fraudsters to gain unauthorized access, even if they have stolen login credentials.

6. Risk-Based Authentication (RBA)

Risk-based authentication dynamically adjusts security measures based on the perceived risk level of a transaction. Low-risk activities, such as logging in from a recognized device, may not require extra verification. However, high-risk actions, such as large-value transactions from a new location, may trigger additional authentication steps.

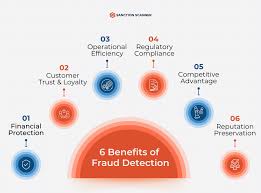

The Benefits of Fraud Prevention Tools for Businesses

Fraud prevention tools offer several advantages to businesses, including:

1. Reduced Financial Losses

Fraudulent transactions result in chargebacks, lost revenue, and fines. By detecting and blocking fraudulent activities in real time, businesses can reduce financial losses and protect their bottom line.

2. Enhanced Customer Trust

Consumers want to feel safe when making online purchases. Businesses that invest in fraud prevention demonstrate their commitment to security, increasing customer trust and loyalty.

3. Compliance with Regulations

Many industries are subject to strict regulations that require businesses to implement fraud prevention measures. Compliance with data security standards like PCI-DSS (Payment Card Industry Data Security Standard) and GDPR (General Data Protection Regulation) helps businesses avoid legal penalties and reputational damage.

4. Improved Operational Efficiency

Manually reviewing transactions for fraud is time-consuming and inefficient. Automated fraud detection tools streamline the process, allowing businesses to focus on growth rather than constantly monitoring for threats.

5. Fewer Chargebacks

Chargebacks can be costly, leading to additional fees and even account restrictions from payment providers. Fraud prevention tools help businesses reduce chargebacks by identifying fraudulent transactions before they are processed.

Choosing the Right Fraud Prevention Tools

When selecting fraud prevention tools, businesses should consider the following factors:

1. Scalability

A good fraud prevention system should be able to scale with your business. As your transaction volume grows, the system should handle increased data without compromising speed or efficiency.

2. Integration with Payment Systems

Fraud prevention tools should integrate seamlessly with existing payment gateways and e-commerce platforms. Businesses should choose solutions that work with their current systems to avoid disruptions.

3. Real-Time Detection Capabilities

The best fraud prevention tools offer real-time detection to stop fraudulent transactions before they occur. Look for solutions with instant alerts and automated response mechanisms.

4. User Experience

Security is essential, but it should not come at the cost of user experience. The right fraud prevention tools balance security and convenience, ensuring that legitimate customers do not face unnecessary barriers while completing their transactions.

5. Customizable Rules and AI Adaptability

Businesses operate in different industries, each with unique fraud risks. Look for fraud prevention tools that allow businesses to customize fraud detection rules and leverage AI that adapts to new fraud tactics.

The Future of Fraud Prevention

As technology evolves, fraudsters continue to find new ways to bypass security measures. To stay ahead, businesses and fraud prevention providers are investing in advanced security technologies.

1. AI-Powered Fraud Detection

AI and deep learning will continue to play a key role in fraud prevention. These technologies will improve accuracy in detecting suspicious activities and reduce false positives, ensuring that genuine transactions are not wrongly flagged.

2. Biometric Authentication

Biometric authentication, such as fingerprint scans and facial recognition, is becoming more common. This technology offers a high level of security while enhancing the user experience.

3. Blockchain Security

Blockchain technology is being explored as a fraud prevention tool due to its ability to provide transparent and tamper-proof transaction records. Blockchain can help verify the legitimacy of transactions and reduce fraud in financial transactions.

4. Global Collaboration on Fraud Prevention

With online fraud being a global issue, businesses, governments, and financial institutions are working together to strengthen security frameworks. Increased collaboration will lead to better fraud prevention policies and improved cross-border transaction security.

Conclusion

Fraud prevention tools are a critical component of secure online transactions. They help businesses detect suspicious activity, protect customer data, and prevent financial losses. As online transactions continue to grow, investing in fraud prevention will be essential for businesses looking to secure their operations and build customer trust.

By leveraging AI, machine learning, biometric authentication, and real-time monitoring, businesses can stay ahead of cyber threats and ensure safe, fraud-free transactions. The future of fraud prevention is constantly evolving, and businesses that adapt to new technologies will be better equipped to combat financial crime in the digital world.